How to Use Insurance for Telehealth Family Visits

Written by Klarity Editorial Team

Published: Jun 22, 2026

Telehealth, the industry term for remote medical care delivered by video or audio, is now covered by most major insurance plans for family visits. Knowing how to use insurance for telehealth family visits correctly means understanding your plan’s coverage rules, submitting claims with the right billing codes, and using accounts like HSAs and FSAs to cut costs. Medicare, TRICARE, and most private insurers all cover virtual visits, but each plan has specific requirements that can trip up families who go in unprepared. This guide breaks down exactly what you need to know in 2026.

What does insurance typically cover for family telehealth visits?

Most insurance plans cover telehealth visits at rates similar to in-person office visits, but the details vary significantly by plan type. Medicare telehealth flexibilities have been extended through december 31, 2027, allowing covered services from the patient’s home in any geographic area. That extension removes the old rural-only restriction that previously blocked millions of families from accessing home-based virtual care.

Private insurers have followed Medicare’s lead. Many states now mandate telehealth coverage and payment parity, meaning insurers must reimburse virtual visits at the same rate as in-person ones. The specific services covered depend on your plan, but primary care, behavioral health, and urgent care are the most commonly included categories.

TRICARE covers telemedicine when medically necessary, with cost-sharing by plan varying based on your status. TRICARE Prime active duty families pay $0 for authorized telemedicine visits. Retired Select families pay standard cost-sharing rates, so the savings depend on which tier your family falls under.

Common telehealth services covered by insurance:

- Primary care and sick visits

- Behavioral health and mental health counseling

- Dermatology consultations

- Chronic disease management

- Prescription refills and medication management

- Pediatric well-child visits (varies by plan)

Common exclusions to watch for:

| Exclusion Type | Why It Matters |

|---|---|

| Out-of-network providers | Claims may be denied or reimbursed at a lower rate |

| Cosmetic consultations | Not medically necessary; rarely covered |

| International telehealth | Most plans only cover visits within the U.S. |

| Experimental treatments | Coverage requires established clinical evidence |

Knowing these exclusions before you book saves you from surprise bills after the visit.

How to use insurance for telehealth family visits: billing and coding

Correct billing is the single biggest factor in whether your telehealth claim gets paid. Incorrect place-of-service coding is the leading cause of telehealth claim denials in 2026. When a provider uses the wrong code, your insurer treats the visit as in-person, which triggers a mismatch and often a denial.

The standard code for a telehealth visit from your home is POS 10 (Place of Service 10). Your provider must use this code, not POS 02 (which applies to telehealth from a non-home location). Some commercial payers also require modifier 95 on the claim to flag it as a telehealth service. If your provider misses either of these, the claim can be denied or flagged for audit.

Your physical location during the visit matters legally and financially. Providers must confirm where each family member is located at the start of every call. This is not just a formality. Insurance reimbursement rules, provider licensure, and billing codes all depend on the patient’s state at the time of service.

Steps to protect your family’s telehealth claims:

- Call your insurer before the first visit and ask specifically about telehealth benefits, not just general coverage.

- Confirm your provider is in-network for telehealth, not just for in-person visits. These can differ.

- Tell your provider your exact location at the start of each call, including your state.

- Ask your provider’s billing team which POS code and modifiers they use for telehealth.

- After the visit, check your Explanation of Benefits (EOB) to verify the claim was processed as telehealth, not as an office visit.

- If a claim is denied, request the denial reason in writing and ask your provider to resubmit with the correct codes.

Families commonly face surprise bills because telehealth visits get billed as in-person visits due to documentation gaps. Catching this early, before the claim is processed, is far easier than appealing a denial.

Pro Tip: Ask your provider’s front desk to confirm the POS code before your appointment ends. A 30-second conversation can prevent a weeks-long billing dispute.

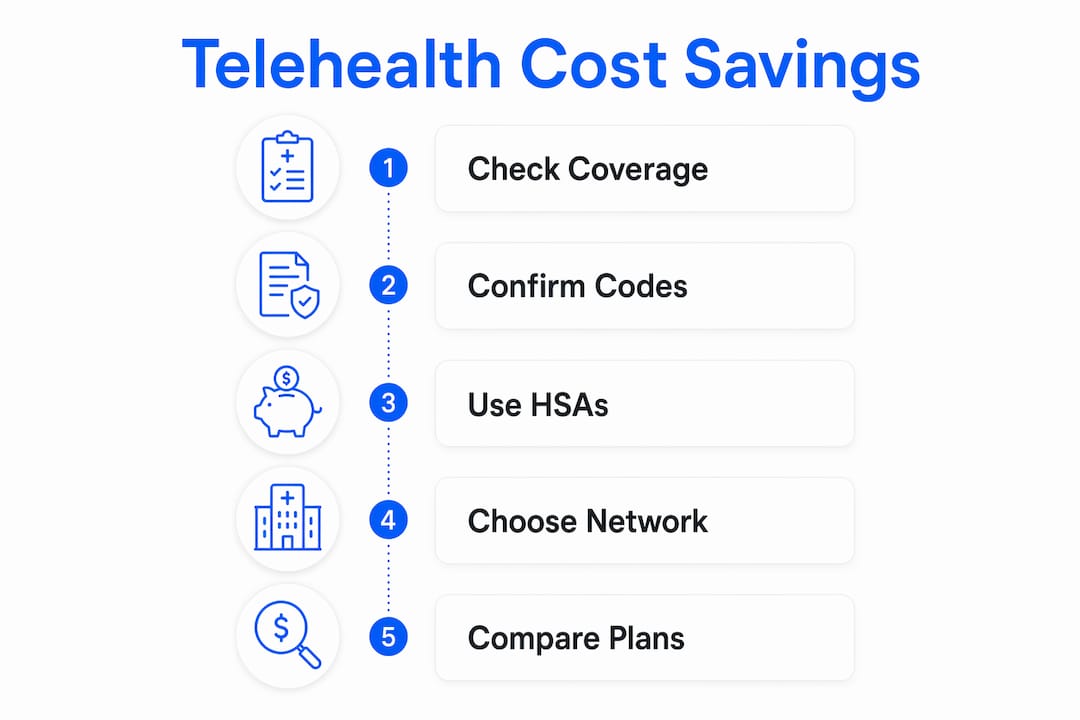

What cost-saving strategies can families use with telehealth insurance?

Understanding your plan’s cost structure prevents the most common financial surprises. Out-of-pocket costs vary with deductibles, copays, and telehealth-specific plan designs, so two families on the same insurer can pay very different amounts.

HSAs and FSAs are among the most underused tools for managing telehealth costs. HSA and FSA accounts are eligible for telehealth expenses including copays and coinsurance. If your family is on a high-deductible health plan (HDHP) paired with an HSA, some plans allow pre-deductible telehealth coverage for certain services. That means you could pay $0 out of pocket for a virtual visit even before you’ve met your deductible.

Key cost-saving strategies for families:

- Use your HSA or FSA card to pay telehealth copays and coinsurance directly. This reduces your taxable income.

- Check for audio-only options. Medicare covers audio-only telehealth through december 31, 2027, primarily for behavioral health. Audio-only visits often carry lower copays than video visits on some private plans.

- Compare telehealth copays to in-person copays. Many plans charge less for virtual visits, especially for primary care.

- Use plan calculators. TRICARE and most large private insurers offer online cost estimators. Run your family’s specific scenario before booking.

- Batch visits when possible. Some plans allow a parent and child to be seen in the same session. Confirm this with your insurer first.

Pro Tip: Call your insurer’s member services line and ask this exact question: “Does my plan cover telehealth visits before I meet my deductible?” The answer directly affects how much you pay per visit.

Families on affordable telehealth plans can also find options that bundle virtual care at predictable monthly rates, which works well for families with frequent healthcare needs.

How should families choose the right telehealth service for their insurance?

Not all telehealth platforms accept all insurance plans, and not all specialties are available on every platform. Behavioral health, primary care, and dermatology are the most widely available telehealth specialties. Subspecialties like cardiology or neurology are less commonly offered via telehealth and may require prior authorization from your insurer.

Provider licensure is a practical barrier many families overlook. A provider must be licensed in the state where the patient is located during the visit. If your family moves or travels, your regular telehealth provider may not be able to see you. The NPI Telehealth directory and your insurer’s provider portal are the two most reliable tools for checking licensure and network status before booking.

Telehealth service comparison: direct-to-employer vs. traditional insurance coverage

| Feature | Direct-to-Employer Telehealth | Traditional Insurance Telehealth |

|---|---|---|

| Cost per visit | Often $0 (employer-paid) | Copay or coinsurance applies |

| Provider network | Employer-contracted platform | Insurer’s in-network providers |

| Specialty access | Usually limited to primary care | Broader, including behavioral health |

| Claim submission | Handled by employer benefit | Patient or provider submits to insurer |

| HSA/FSA eligibility | Varies by employer plan | Generally eligible |

Families on TRICARE face an additional layer of complexity. Active duty dependents and retired family members fall under different cost-sharing tiers. Using TRICARE’s plan calculators or calling member services before scheduling prevents billing surprises across a mixed-eligibility household.

For pediatric telehealth visits, parents should verify that the platform’s providers hold pediatric credentials and that the child’s specific plan covers virtual well-child visits. Some plans restrict telehealth well-child visits to certain age groups.

What to confirm before booking any family telehealth visit:

- Provider is licensed in your state

- Provider is in-network for telehealth specifically

- Your plan covers the visit type (behavioral health, primary care, etc.)

- Prior authorization is not required

- The platform accepts your insurance and processes claims directly

Key Takeaways

Families who verify billing codes, confirm in-network status, and use HSAs or FSAs correctly will get the most value from their insurance for telehealth visits.

| Point | Details |

|---|---|

| Medicare extended through 2027 | Home-based telehealth is covered in any geographic area through december 31, 2027. |

| POS 10 is the critical code | Providers must use POS 10 for home telehealth visits to avoid claim denials. |

| HSAs and FSAs reduce costs | Use these accounts to pay telehealth copays and coinsurance with pre-tax dollars. |

| Verify in-network status | Telehealth network status can differ from in-person network status on the same plan. |

| TRICARE varies by tier | Active duty Prime families pay $0; retired Select families pay standard cost-sharing rates. |

What I’ve learned navigating telehealth insurance for families

The biggest mistake I see families make is assuming their insurance works the same way for telehealth as it does for in-person visits. It does not. The billing infrastructure is different, the network rules can differ, and the location requirement catches people off guard every time.

The policy side adds another layer of uncertainty. Congress has extended pandemic-era Medicare telehealth flexibilities multiple times rather than making them permanent. The current extension runs through 2027, which gives families a stable window. But families relying on Medicare should watch for legislative updates after 2027, because the rules could change again.

The families who navigate this best are the ones who treat the insurer as a partner, not an obstacle. One phone call before the first visit, asking specifically about telehealth benefits and billing codes, prevents the majority of claim denials I’ve seen. Providers appreciate it too. When a patient confirms their location and asks about POS codes upfront, the billing team has everything they need to submit a clean claim.

Telehealth is genuinely one of the most convenient healthcare options available to families right now. The access it provides, especially for mental health telehealth and pediatric care, is real and meaningful. Getting the insurance side right is the only thing standing between your family and that access.

— Guorui

Helloklarity makes family telehealth coverage straightforward

Helloklarity connects families with over 1,000 licensed providers across mental health, primary care, and weight loss, with same-day appointments available in most cases. The platform accepts major insurance plans and health savings accounts, so you can use your existing coverage without navigating a separate billing process.

Patients can see a provider within 24 hours, and self-pay options start at $49 for those whose insurance does not cover a specific service. Helloklarity’s provider network is searchable by state, making it easy to confirm that your provider is licensed where your family is located. Browse available telehealth services to see what your plan may cover, or find a provider near you to get started today.

FAQ

Does insurance cover telehealth visits for the whole family?

Most major insurance plans, including Medicare, TRICARE, and private insurers, cover telehealth visits for eligible family members. Coverage details, including copays and which services qualify, vary by plan and family member status.

What billing code should my provider use for a home telehealth visit?

Providers should use POS 10 (Place of Service 10) for telehealth visits conducted from the patient’s home. Using the wrong code is the leading cause of telehealth claim denials in 2026.

Can I use my HSA or FSA for telehealth copays?

Yes. HSA and FSA accounts are eligible for telehealth expenses including copays and coinsurance. If your family is on an HDHP with an HSA, some plans cover telehealth before you meet your deductible.

Does Medicare cover audio-only telehealth visits?

Medicare covers audio-only telehealth through december 31, 2027, primarily for behavioral health services. Patients do not need an initial in-person visit before starting mental health telehealth under the current federal extension.

How do I avoid surprise bills from telehealth visits?

Call your insurer before your first visit and confirm telehealth benefits, in-network status, and whether prior authorization is required. After the visit, review your Explanation of Benefits to verify the claim was processed as telehealth, not as an in-person office visit.

Recommended

- Does Insurance Cover Telehealth? What Every Major Plan Actually Covers In 2026 | Klarity Health, Inc

- Affordable Telehealth Plans For Families In 2026

- How Telehealth Cuts Your Out-of-Pocket Healthcare Costs

- What Is A Telehealth Visit? How It Works, What It Costs, And How To Start | Klarity Health, Inc

Get expert care from top-rated providers

Find the right provider for your needs — select your state to find expert care near you.

Related posts

— Monday to Friday, 7:00 AM to 4:00 PM PST

Join our mailing list for exclusive healthcare updates and tips.

— Monday to Friday, 7:00 AM to 4:00 PM PST